On 24 August 2021, the Mauritius Revenue Authority (“MRA”) issued a Statement of Practice (“SOP”) for Trusts and Foundations.

The SOP is in line with the amendments brought by the Finance (Miscellaneous Provisions) Act 2021 (“The Finance Act”), which brought about significant amendments to the declaration of non-residence for tax purposes for Trusts and Foundations.

As a reminder, section 46 subsection 3 and section 49A subsections 2 and 3 were repealed.

These subsections provided that when a qualifying trust/foundation deposits a declaration of non-residence for any income year with the tax authority within 3 months of the expiry of the income year, the trust/foundation would be exempt from income tax in respect of that income year.

Interested in Learning More About Taxation of Trusts?

Register Your Interest To Attend Our Upcoming Training Here!

1. SOP’s Objective

The MRA SOP seeks to clarify the application of sections 73A and 116 of the Income Tax Act (“ITA”) pertaining to Trusts and Foundations in light of the amendments in the ITA. The SOP reference is SP 24/21.

2. The Basics

A. Definition

Trust and foundations fall within the definition of “company” defined in section 2 of the ITA.

The Trust Act and section 2 of the ITA govern trusts in Mauritius. A “trust” means a trust recognised under the laws of Mauritius.

A foundation has the same meaning as in the Foundations Act.

B. Parties

There are 3 main parties involved in a trust, namely settlor, trustee and beneficiary.

According to the Trust Act:

- A settlor means a person who provides trust property or makes a testamentary disposition on trust or to a trust.

- A Trustee means a person who holds or has vested in him, or is deemed to hold or have vested in him, property of which he is not the owner in his own right, with a fiduciary obligation to hold, use, deal or dispose of it –

(a) for the benefit of any person (a “beneficiary”) whether or not yet ascertained or in existence.

(b) for any purpose, including a charitable purpose, which is not for the benefit only of the trustee; or

(c) for such benefit as is mentioned in paragraph (a) and also for any such purpose as in mentioned in paragraph (b)

- A Beneficiary means a person, whether natural or corporate, entitled to benefit under a trust or in whose favour a power to distribute trust property may be exercised.

- The maximum trustee for a trust is 4, and at least one shall be a qualified trustee. A qualified trustee means a management company or such other person resident in Mauritius who is authorised to provide trusteeship services.

There are 3 main parties involved in a foundation, namely founder, executor and beneficiary.

According to the Foundation Act:

- A Founder means a person who endows a Foundation with its initial assets.

- An executor means a person named in a will, or nominated by the founder, to carry out the directions of the will and includes the executor’s duly appointed lawful agent in the case of a foreign will.

- A beneficiary means a person entitled to benefit under a Foundation or in whose favour a power to distribute any Foundation property may be exercised.

3. Liability To Tax

As a general rule, the income of Mauritius Trust and Foundations is subject to income tax at the rate of 15%.

Before the Finance Act 2021, if a trust was deemed to be a qualified trust. It could file a declaration of non-residence with the Director-General/tax authority within 3 months after the expiry of the income year. As a result, it was exempt from income tax in respect of that year.

The conditions to be a qualified trust are where in an income year, a trust:

- Of which the settlor is a non-resident or holds a Global Business Licence under the Financial Services Act

- Of which all the beneficiaries appointed under the trust are, throughout an income year, non-residents or holds a Global Business Licence under the Financial Services Act

- Which is a purpose trust under the Trust Act and whose purpose is carried out outside of Mauritius.

Before the Finance Act 2021, this was similarly applied to foundations.

A foundation that met either of these conditions was considered as a qualified foundation:

- The founder is a non-resident or holds a Global Business Licence under the Financial Services Act; and

- All the beneficiaries appointed under the terms of a charter or a will are, throughout an income year, non-resident or hold a Global Business Licence under the Financial Services Act.

A qualified foundation could deposit a declaration of non-residence for any income year with the Director-General within 3 months from expiry of the income year. As a result, it was exempt from income tax in respect of that year.

Interested in Learning More About Taxation of Trusts?

Register Your Interest To Attend Our Upcoming Training Here!

4. Grandfathering

Following the repeal of the two subsections, the above exemption will no longer be available except for trusts and foundations set up before 30 June 2021.

These entities can avail themselves of the exemption up to the year of assessment 2024/2025.

Trusts and foundations having an income year starting on or after 31 December 2024 will not benefit from this grandfathering provision.

Note:

During the grandfathering period, the grandfathered trust/foundation cannot benefit from the exemption regarding new assets or activities such as intellectual property assets acquired and income from specific assets or projects started after 30 June 2021.

5. Trusts and Foundations Resident in Mauritius

The definition of residence is set out in section 73 of the ITA.

We have reproduced the relevant section below:

Trust and foundations that are considered residents according to the definition of residence set out in section 73 of the ITA will be liable to tax in Mauritius on their worldwide income at the rate specified in Part IV of the First Schedule the ITA that is, 15%.

6. Non-Resident Trusts and Foundations

1. Residency Concept

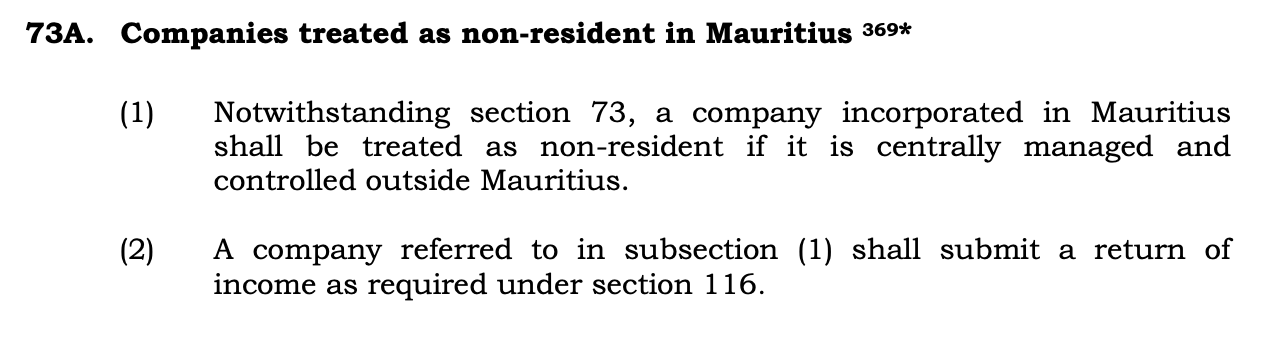

A company incorporated in Mauritius is non-resident if it is centrally managed and controlled outside Mauritius in accordance with section 73A of the ITA.

We have reproduced section 73A of the ITA below:

On the basis that trusts and foundations fall within the definition of ‘company’ in accordance with section 2 of the ITA, they are deemed non-resident if their central management and control take place outside Mauritius.

2. Central Management and Control

The SOP clarifies the concept of central management and control for trusts and foundations. It states that:

A. Trust:

A trust would have its central management and control in Mauritius when:

- The trust is administered in Mauritius, and a majority of the trustees are resident in Mauritius;

- The settlor of the trust was resident in Mauritius at the time the instrument creating the trust was executed or at such time as the settlor adds new property to the trust; and

- A majority of the beneficiaries or the class of beneficiaries appointed under the terms of the trust are residents in Mauritius.

A foundation would have its central management and control in Mauritius if:

- The founder is resident in Mauritius; and

- A majority of the beneficiaries appointed under the terms of a charter or will are residents in Mauritius.

Interested in Learning More About Taxation of Trusts?

Register Your Interest To Attend Our Upcoming Training Here!

7. Income Derived From Mauritius

The SOP provides that a trust or foundation that, throughout an income year, is non-resident, shall be liable to tax only on its chargeable income attributable to its Mauritian source income at the rate specified in Part IV of the First Schedule the ITA that is, 15%.

8. Exempt Body

A foundation or trust whose exclusive purpose or object is of a charitable nature will be exempt from tax in Mauritius in accordance with item 1 of Part I of the second schedule to the ITA.

9. Partial Exemption

Any foundation or trust may claim partial exemption on such categories of income specified under Sub Part B or Sub Part C of the Second Schedule to the ITA subject to satisfying the conditions prescribed relating to the substance of their activities.

10. Annual Return of Income

Any foundation and trust shall submit an annual return of income. This is in accordance with section 116 of the ITA, which provides for the return of income by companies.

Interested in Learning More About Taxation of Trusts?

Register Your Interest To Attend Our Upcoming Training Here!

Sharpen Your Tax Skills